Understand the current development status of China's cable industry and find opportunities for replication and transfer

ONE. Introduction

The wire and cable industry has a history of more than 100 years. China began manufacturing wires and cables in the 1930s and has experienced nearly eight decades of development . It has become a major wire and cable manufacturing country in the world.There are nearly 10,000 wire and cable manufacturing companies in China . After rapid development, the industry has seen problems such as overcapacity, price competition, and quality issues, which have affected the high-quality development of the industry. Since the "Aokai incident" in Xi'an in 2015, some companies with poor quality and innovation capabilities have been eliminated, and the entire industry is facing a great test.

TWO. Cable Status in Developed Countries

1. Overview of the development of international wire and cable

In recent years, an obvious trend is that the economic growth of emerging countries such as Asia is relatively fast, and the production center of the world's wire and cable has shifted to Asia, driving the rapid development of the wire and cable industry in countries such as China, Vietnam, the Philippines and Egypt in the Middle East. At the same time, due to the unification of Europe and relatively low manufacturing costs, the growth of wire and cable manufacturing in Central and Eastern Europe is also quite rapid.

The demand for wire and cable markets in Africa, the Middle East and even Southeast Asia is booming, which is in sharp contrast to the decline in the European and East Asian markets. With the rapid development of these emerging markets and the acceleration of infrastructure construction, the sales and investment opportunities of wire and cable have attracted great attention in the industry.

International wire and cable research data found that market demand in developed economies such as Europe and East Asia is accelerating differentiation. Due to the economic recovery after the 2009 financial crisis, the demand for wires and cables in the United States has also achieved a slight year-on-year increase. The slowdown in the EU's economic development has also affected the demand for wires and cables. According to the "2016-2020 China Wire and Cable Industry Investment Analysis and Prospect Forecast Report", the overall global demand for wires and cables has achieved an average annual growth rate of 3.2%. China has become one of the world's largest consumers of wires and cables.

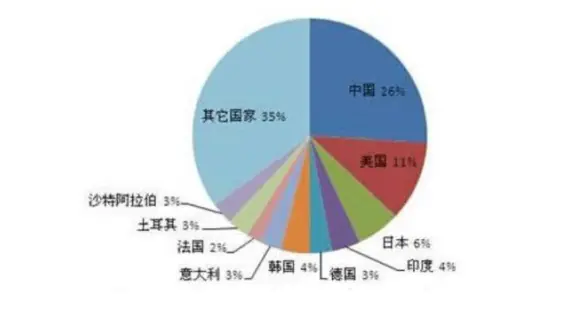

Figure 1 Proportion of wire and cable output value in major countries in the world

Judging from the trend of technological development in the world cable industry, the future development direction is: large capacity, ultra-high voltage, oil-free, short-circuit resistance, high reliability, and maintenance-free. At present, cross-linked cables of various voltage levels have gradually replaced traditional oil-filled paper insulated power cables, and the application of high-voltage and ultra-high-voltage cross-linked cables is becoming more and more extensive. Europe, the United States and Japan currently have higher and higher requirements for the cables used, and have strictly prohibited the use or import of non-environmentally friendly cables. With the promulgation of the EU RoHS directive, the large-scale adoption of ecological and environmentally friendly wires and cables has become a global trend.

2. Main characteristics of the current international wire and cable industry

(1) Asia becomes the world's largest wire and cable concentration region

In 2010, the overall scale of the global wire and cable industry was 37% in the Asian market, nearly 30% in the European market, 24% in the American market, and 9% in other markets. According to the output of copper conductors and the country of origin, China, the United States, Japan, Germany, and South Korea occupy the top five positions in the world. China's output accounts for 30.5% of the global share, of which the output of mainland China accounts for 27.6%, and its annual growth rate ranks first among all countries and regions in the world. This pattern has not changed.

(2) Developed countries have high industrial concentration

After years of development, the wire and cable industry in developed countries has seen a significant increase in industry concentration, especially in the face of fluctuations in raw material prices, as small businesses have gradually withdrawn from the market: four American manufacturers control 93% of the output value of copper cables and 85% of the output value of optical fiber cables; seven Japanese companies account for 86% of the country's sales; 12 British companies account for more than 95% of the country's sales; the five largest companies in France have monopolized the French market's turnover; and the European market is mainly monopolized by Italy's Prysmian and France's Nexans.

(3) Europe continues to maintain its competitive advantage

In terms of regions, Europe has always been in the leading position in the global wire and cable manufacturing field, mainly due to the heavy investment in product research and development by France's Nexans, Britain's BICC and Italy's Prysmian; on the other hand, 70% of the production cost of wire and cable depends on raw materials, and labor costs are less than 10%. Therefore, Asia's labor cost advantage is not fully reflected in the global wire and cable industry competition landscape.

(4) The global cable market is becoming mature and the growth rate is slowing down

In terms of market supply and demand, the global wire and cable market is becoming mature and growing slowly. International and domestic tracking and analysis of the development of the wire and cable industry show that as long as a country or region's economy is growing, especially in the process of industrialization and urbanization, its wire and cable industry growth will be above the GDP growth rate. China's per capita GDP level is far lower than that of developed countries, and its per capita cable consumption level is far lower than that of moderately developed countries in Europe, and even lower than that of developing countries such as Latin America. The market potential of China's wire and cable consumption still has great room for development.

(5) Environmental protection has become the development trend of global wire and cable products

In terms of products, environmental protection has become the external pressure and development trend faced by cable manufacturers around the world in recent years. The United States, Japan, and Europe are in the world's leading position in the research and development and manufacturing of environmentally friendly cables, and their production technology is relatively mature. The ROHS directive formulated by the European Union requires that from July 1, 2006, the use of harmful substances such as lead, mercury, cadmium, hexavalent chromium, polybrominated diphenyl ethers and polybrominated biphenyls in new electronic and electrical equipment on the market is prohibited; in Japan, after Fujikura Cable Company successfully developed environmentally friendly cables, it actively promoted the government to issue environmentally friendly cable standards. Subsequently, major Japanese electrical companies also successively required that from March 2006, the wires and cables used in various electrical appliances must pass relevant environmental certification.

3. Recent developments and trends of international wire and cable companies

(1) Mergers and reorganizations to gain strategic advantages and integrate businesses to improve competitiveness

The four largest cable companies in the former Western European market: Alcatel of France, Pirelli of Italy, Siemens of Germany, and BICC of the United Kingdom, etc., have been reorganized. Alcatel only retained the optical fiber and cable business, and the metal cable business was separated from the group to form Nexans of France. Nexans has become one of the largest multinational cable companies in Europe and even the world by acquiring many cable companies; Pirelli acquired Siemens' power cable business and purchased the cable business of the original BICC and other companies from General Cable of the United States, becoming the second largest multinational cable company in Europe. After that, Pirelli was acquired by Prysmian of Italy; while Siemens and BICC have basically withdrawn from the cable market. The Dutch Treka Company was originally a small-scale general wiring manufacturer in Northern Europe. It has become the largest company in the Nordic market through continuous mergers and acquisitions of small and medium-sized enterprises in Europe and other regions. After the adjustment and adaptation of these mergers and reorganizations, the European cable industry has been revived. Strategic reorganization not only enables these companies to selectively enter or exit the field of cable manufacturing, but also rapidly increase the market share of their main businesses in the world, making them giants in the international cable industry. The restructuring of the European cable industry also benefited from the advancement of European unification and the transformation of industrial policies of the EU authorities and governments of various countries. The implementation of these policies played an important catalytic role in the restructuring of the wire and cable industry. There are also similar strategic restructuring activities in the US market.

The Japanese wire and cable industry hit rock bottom in the late 1990s. At the beginning of this century, business integration between companies began, which gradually pushed the cable industry into a trough. For example, in the field of high-voltage power cable manufacturing, Sumitomo Corporation and Hitachi established a joint venture J-Power; Furukawa Corporation and Fujikura Corporation established Viscas; Showa Corporation and Mitsubishi Corporation established Exsym. Similar situations also occurred in Japan's winding wire and building wire manufacturing fields. In 2016, Japan's VISCAS began to reorganize its business. Furukawa Electric acquired the company's underground and submarine transmission cable business, and Fujikura acquired the company's distribution line and overhead transmission cable business. Through this split and reorganization, the advantages of the two companies were flexibly utilized to further develop these two businesses.

(2) Relocating production bases to obtain excess returns

In recent years, many large international cable companies have shifted their production focus to Asia and other regions, especially China. The wire and cable factories established by foreign capital in China cover a wide range of products, involving almost all product fields, and have made considerable progress. For example, the 110~220kV cross-linked cables of Shenyang Furukawa, Baosheng Prysmian and Hangzhou Huaxin occupy a leading position in China. With a considerable market share, the French company Nexans' special cables and transportation cables have continuously won bids in some key domestic projects due to the influence of its brand.

(3) Continuous innovation creates value

Foreign companies attach great importance to continuous innovation. For example, Prysmian's innovation activities are not limited to high value-added business, product research and development and improvement, but also pay attention to continuous improvement and optimization in manufacturing, supply chain and service. Through systematic innovation activities, it aims to increase the share of the cable market and improve the company's adaptability to changes in the external environment. In 2007, its group sales were 5.118 billion euros, and its R&D investment was 45.5 million euros, an increase of 8.8% over the previous year. It has 7 R&D centers around the world and more than 3,000 patents in 6 countries. In 2006 alone, Prysmian registered 258 patents. At the same time, foreign companies attach great importance to tracking and researching cutting-edge technologies in order to seize the commanding heights of technology and market opportunities. For example, in the research of superconducting cable technology, the top ten applicants for patent applications are Japanese companies such as Sumitomo, Furukawa, Tokyo Electric Power, Fujikura, Toshiba, Mitsubishi, Siemens, Pirelli, Nexans and American Superconductor.

(4) Specialized products monopolize specialized markets Among

European, American and Japanese wire and cable companies, in addition to some well-known large companies that produce a wide range of products, there are also some specialized companies that focus on manufacturing a certain type of product. Although they are not as eye-catching as large companies in the industry, they dominate their professional fields. For example, in the field of cable manufacturing for oil and gas exploration and offshore engineering, which has seen rapid market growth in recent years, although cable giants such as Nexans also produce such products, the global market leader is a medium-sized American company, Amer Cable. Due to its focus on the research and development of special cable products, its emphasis on the engineering application of cables, its ability to solve technical problems in engineering applications, and its advantages of timely delivery, it has achieved remarkable results in the cable product market in special fields.

4. Current status and development trend of cable materials in the world

With the development of the world's cable industry, the demand for various cable materials is also growing.

(1) PE cable material

PE was used for communication cables internationally as early as the 1940s. In the mid-to-late 1990s, PE cables had already occupied an important position in PE products. In recent years, with the increasing calls for environmental protection, PE is gradually replacing PVC internationally, resulting in an increase in the consumption of PE cable resins year by year.

1) PE high-speed extrusion communication cable material

At present, high-density polyethylene (HDPE) or medium-density polyethylene (MDPE) is generally used as communication insulation material in the world. HDPE has good mechanical strength and electrical properties, especially high toughness, which fully meets the requirements for the use of insulation materials. Since the mid-1970s, most of the insulation layers of urban telephone cables have been made of HDPE.

2) XLPE cable material

Internationally, XLPE production technology is mainly divided into three categories: radiation cross-linking mainly produces cables for electrical equipment; silane cross-linking uses silane as a cross-linking agent to cross-link PE under the action of a catalyst; chemical cross-linking uses low-density polyethylene (LDPE) as a base material and organic peroxide as a cross-linking agent. It is suitable for cables used under high temperature, high pressure, high frequency and other conditions, and can be used to manufacture medium and high voltage power cables, aviation cables, control cables, etc.

3) Flame retardant PE cable material

In the early 1980s, low-smoke halogen-free flame-retardant cable materials were developed internationally . By the late 1980s, the second generation of halogen-free flame-retardant plastics for wires and cables had been developed. Compared with the first generation of products, the second generation of halogen-free flame-retardant plastics has improved flame retardancy, smoke generation, toxicity, corrosion, mechanical properties, and electrical properties, and its high-speed extrusion performance is a major feature.

4) Shielded cable material

Shielded cable material is a semi-conductive composite material used in cables to protect the main insulation layer from being damaged. According to IEC60502, PVC and EPDM insulated cables with rated voltages above 1.8/3.0kV, and cables with rated voltages above 3.6/6.0kV, must use inner and outer semi-conductive shielding layers.

Many international polyolefin manufacturers have developed and produced semi-conductive shielding materials for XLPE cables, such as UCC in the United States, Honjibu Kosan Co., Ltd., and BP in the United Kingdom.

(2) PVC cable material

Among the insulation and sheath materials of wires and cables, PVC is relatively cheap, has excellent mechanical properties, and is easy to process, making it the most widely used material in the wire and cable industry for a long time. At the end of the 20th century, the environmental problems of PVC materials were widely recognized, and some developed countries have proposed legislative proposals to restrict or completely ban the use of PVC cables. Data show that the amount of PVC used in the cable field in Western European countries was 441k tons in 1994, accounting for 58% of the polymers used in cables, while in 2000, the total amount of PVC used in the Western European cable industry was 398k tons, accounting for 48% of the polymers used in cables, and both the total amount and the proportion are on a downward trend. In recent years, there has been a strong trend to control and ban the use of PVC materials.

Although there is an increasing call to replace PVC materials with halogen-free materials, PVC itself has advantages that cannot be replaced in the short term (such as low price, good flame retardancy, simple processing equipment and process, wide adjustable hardness range, good electrical insulation, oil resistance, chemical resistance, etc.), so it is not realistic to completely ban the use of PVC worldwide in the short term.

(3) PP cable material

PP is widely used in power cable overhead lines and electrical equipment cables due to its superior mechanical properties, electrical properties, wear resistance, chemical resistance, especially oil resistance. PP was used for wire and cable insulation abroad in the 1960s. By the mid-to-late 1990s, the amount of PP in the United States had reached more than 10kt, accounting for a relatively important share in the total amount of PP. British BP, 13-Benzibu Kosan, German Bayer and other companies all have PP cable material brands, but the most PP wire and cable brands developed in the United States, and ProfaxSE191 is the best. Due to the requirements of low temperature resistance and flexibility, the PP used in foreign cables is ethylene-propylene block copolymer.

THREE. Status of China's Cable Industry

- Output value of wire and cable industry

During the period of 2016-2020 , the overall economy of the cable industry has achieved sustained and stable growth, and the development of the industry in the central and western regions has further accelerated, laying a good economic foundation for the subsequent development of the industry.

2. Production capacity status

With the rapid development of China's national economy, the wire and cable industry, known as the "nerves" and "blood vessels" of the city, has grown into the second largest industry in China's machinery industry, second only to automobiles. According to statistics, there are currently as many as 8,000 large and small enterprises in China's wire and cable industry, of which there are about 2,800 large and small enterprises, and there are only more than 50 cable companies that can truly bid for some major national projects. From the perspective of the types and grades of products produced, most of the main products of the 8,000 large and small wire and cable companies in China are products with low technical content and product added value.

With the acceleration of the process of global economic integration, foreign capital has gradually entered China's cable industry. China 's cable industry has shifted from a single economy to a diversified ownership system, and private enterprises have become the most important economic force in the cable industry. There is a serious overcapacity in production: the annual production capacity of imported and domestic copper rod continuous casting and rolling production line equipment exceeds 10 million tons; the annual production capacity of upward-drawn continuous casting copper rod production line equipment is about 6 million tons; the annual production capacity of electrical aluminum rod continuous casting and rolling production unit equipment is about 4.5 to 5 million tons; the annual production capacity of catenary medium voltage (including some 110kV) power cable production lines exceeds 400,000 km; the annual production capacity of tower-type high voltage/ultra-high voltage power cable production lines is 45,000 km; the annual production capacity of optical fiber drawing is 66 million core km.

3. Current status of domestic product varieties

In China Power cable category: According to the IEC62067 (GB/T22078-2008) standard requirements, nearly ten cable manufacturers have produced and trial-produced 290/500kV cross-linked polyethylene insulated power cables, and about 8 companies have passed the pre-qualification test. In addition, the 290/500kV cross-linked polyethylene insulated power cables and accessories produced in China have been safely used in the Beijing urban power grid this year; 127/220kV passed the type test in August 1997 by Shenyang Guhe Cable Co., Ltd., and passed the qualification test in October 1999 by TBEA Luneng Taishan Cable Co., Ltd. Since then, nearly 30 companies have passed the type test and pre-qualification test. Now, the annual usage of power grid companies and user projects is about 1500~2000km. The 110kV high-voltage XLPE cable produced by 64/110kV Shenyang Cable Factory passed the joint qualification of the former Ministry of Machinery and Electronics and the Ministry of Energy as early as December 1991.

Since then, nearly 40 companies have passed the type test. Now, the annual usage of power grid companies and user projects is about 6,000 to 7,000 km. The production capacity of medium-voltage cross-linked polyethylene insulated power cables is huge. They are not only used in domestic projects in China , but also exported. The submarine power cables that can be produced and have passed the test include single-core and three-core 126/220kV, single-core and three-core 64/110kV cross-linked polyethylene insulated submarine power cables and have been used. 500kV cross-linked polyethylene insulated submarine power cables are under trial production. Medium-voltage cross-linked polyethylene insulated submarine power cables have been in use for more than ten years.

The production capacity of oil-paper and oil-filled power cables has been almost eliminated.

Electrical equipment wires: China sells about 250-300 billion RMB worth of IEC60245 and IEC60227 products each year; automotive wire production capacity is in excess, and technical requirements can meet the product requirements of major global automotive companies; mining cable production capacity is in excess, and competition is becoming increasingly fierce in the context of advocating the development and use of clean energy; marine cable production capacity is in excess, and Chinese domestic manufacturers and foreign companies are competing for the same market in China; submersible pump cables can basically be domestically produced; the production and inspection technology of cables for third-generation nuclear power plants has been fully mastered; the production, technology and testing of torsion-resistant cables for wind power generation and photovoltaic power generation cables fully meet the requirements of technological development, and there is already a surplus phenomenon.

Bare wire products: It can produce overhead wire products that meet the requirements of 1000kV AC and DC transmission, and has been used. The production capacity is also in excess, but there is still a contradiction between delivery time and production capacity.

Winding wire products: The winding wire production industry has been basically integrated, and large-scale enterprises have been formed, which can fully meet domestic demand, but are in a state of low profit.

Optical and cable products for communications: The optical cable product manufacturing industry has been basically integrated, and large-scale enterprises have been formed, which can fully meet domestic demand, and the favorable demand will continue for several years.

4. Domestic product demand

In China At present, the wire and cable industry as a whole is in a state of overcapacity:

(1) The national production capacity of high-voltage and overvoltage cables is about 45,000 km/year, while the actual demand is about 11,000 km/year, and the operating rate is about 30% to 35%;

(2) The national production capacity of medium-voltage cables is about 360,000 km/year, while the actual demand is about 150,000 km/year, and the operating rate is about 40% to 45%;

(3) The national production capacity of low-voltage cables is about 700,000 km/year, while the actual demand is about 370,000 km/year, and the operating rate is about 50%;

(4) The national production capacity of high-voltage cable accessories is about 200,000 sets/year, while the actual demand is about 70,000 to 80,000 sets/year, and the operating rate is about 40%;

(5) The annual production capacity of imported and domestic copper rod continuous casting and rolling production line equipment exceeds 10 million tons, and the annual production capacity of upward continuous casting copper rod production line equipment is about 6.5 million tons, and the demand is about 6-8 million tons;

(6) The annual production capacity of electrical aluminum rod continuous casting and rolling production equipment is about 6.5 million tons, and the demand is about 3 million to 4 million tons;

(7) The annual production capacity of optical fiber drawing is greater than 66 million core km;

(8) The annual production capacity of optical cables is greater than 90 million core cables;

(9) The production capacity of electrical equipment lines cannot be counted, and the overcapacity is quite serious.

5. Development opportunities

Market resources will gradually concentrate on brand-advantaged enterprises, and the premium of brands will gradually promote competition from price competition to a higher level of product quality, technical performance, service experience and comprehensive cost-effectiveness; advantaged enterprises will rise rapidly, the gap will widen, large enterprises will become stronger, and small and medium-sized enterprises will develop towards specialization and innovation.

The role of the international market in the market structure is enhanced. Facing the double squeeze of the technological advantages of high-end products in Europe, the United States and Japan and the low-end and medium-end products in low-cost countries; promoting enterprises going abroad to strengthen themselves and continuously improve their international competitiveness; export products gradually change from low value-added products to medium and high value-added products.

Future development opportunities are mainly reflected in the following aspects

(1) "One Belt, One Road" strategy. The proposal of this strategy has undoubtedly boosted the entire infrastructure construction, and infrastructure interconnection is the priority area of this strategic construction. Among them, the cable industry will benefit the most. Whether it is the construction of cross-border optical cables and other communication networks that directly benefit cable companies in the "One Belt, One Road" vision and action documents, or the construction of cross-border power and transmission channels, as well as hydropower, nuclear power, wind power, solar energy and other indirect stimulation of cable demand, this will be a major historical opportunity for cable companies.

(2) "Military-Civil Integration" strategy. This project will bring certain opportunities to cable companies, but companies that really bring benefits should have certain technical strength and production equipment, fully realize the particularity and diversity of military products, and have certain technical strength to participate in it. This project will have an impact on the development of the industry and the industry's contribution to national defense.

(3) Supporting new energy Through the changes in the cable industry in the past two years, it can be seen that the new energy field has a relatively large development space, such as photovoltaic power generation, wind power generation, nuclear energy support, etc.

(4) Supporting emerging industries such as electric vehicles, robotics industry, port shore power, airports, data transmission (digital, image transmission), security engineering, etc.

(5) Supporting cables for small urbanization projects.

(6) Cables for islands meet the requirements of marine island development, such as rodent-proof, sunlight-resistant, and seawater-resistant.

(7) Port machinery meets the dynamic cables of port machinery and realizes localization.

(8) High-end irradiated low-smoke and halogen-free cables replace PVC insulated home decoration cables, flame-retardant, fire-resistant, and low-smoke and halogen-free cables replace ordinary cables to meet special requirements. IV

FOUR. Problems in the cable industry

1. The current development status of industrial clusters is the trend of convergence within the industry. Influenced by location conditions, regional cultural environment, etc., the initial local imitation and copying, as well as natural growth, mostly formed a structure and foundation of enterprise isomorphism, capital uniformity, product and market homogeneity; due to the lack of healthy internal interaction and external stimulation, there is a general lack of strategic cooperation in division of labor and cooperation in the production chain and complementary production capacity between leading enterprises and small and medium-sized enterprises; when the agglomeration develops to a certain scale and market, talent and other factor resources become tight, the agglomeration area tends to be mutually closed and engage in homogeneous competition; the demonstration effect of leading enterprises is not significant, the quality of small and medium-sized enterprises is difficult to improve, and the synergistic effect of enterprise agglomeration is difficult to exert.

2. The low-end products are in excess but of poor quality, and the high-end products are in short supply, resulting in weak international competitiveness, which is mainly manifested in the following aspects:

(1) The serious overcapacity environment has led to excessive low-price competition, and severe cost pressure often affects product quality;

(2) In the field of traditional products with large volume and wide coverage, it is still common to see that the quality management system of enterprises is not sound and the quality control is not strict;

(3) The quality quality of employees is not high, training is insufficient, and full participation in quality improvement is insufficient;

(4) There are not many enterprises that mainly adopt the common product standards and establish high standards (higher than national standards or international advanced standards) for internal control;

(5) The level of quality management informatization is low, and the capabilities

of online automatic collection of quality data, networking of inspection and testing equipment, and online collaboration of quality business in the industrial chain need to be established and improved; (6) The ability to analyze and apply basic quality data is not high, and the application of quality tools is still relatively basic. The ability to apply quality prevention tools and innovate quality tools is not high;

(7) Insufficient research on mass production processes, unstable process control of high-end products, poor quality stability, low reliability, and high production costs affect the market acceptance of domestic new technologies and new products and the effective expansion of application areas, and restrict the improvement and improvement of technology.

3. There are no characteristic products and internationally influential enterprises in the region.

4. The role of the cluster area has not been brought into play. Most of the enterprises are small and comprehensive, and there is no division of labor in product varieties.

5. Resource waste. The regional advantages have not been brought into play, and the advantages of sharing common equipment resources have not been shared.

6. Due to the rapid imitation and low cost in the region, there is a shortage of cable products, such as the lack of optical cables and communication cables in the region.

FIVE. Suggestions on development countermeasures

Although wire and cable are traditional industries and supporting industries, as long as electricity exists, wire and cable must be used. Therefore, the wire and cable industry is an immortal industry. The key is how to do this industry well. For the main industry of a region, more attention should be paid to its healthy development. In today's rapid changes, it is recommended to pay attention to the following matters in the development process:

1. Do a good job in top-level design

. As local competent departments, they should guide local enterprises to plan integration roadmaps in accordance with the development laws of the industry; plan from a strategic height. Guide the transformation of excess production capacity; with the business thinking of "century-old stores", focus on product quality and brand building; from the perspective of production efficiency, enterprises in the region should divide the work and cooperate in product varieties and subdivided processes; in the raw material supply chain, enterprises in the region should cooperate.

2. The production method should be transformed and

equipment should be updated: accelerate the upgrading of production equipment. Some equipment is outdated, does not meet environmental protection requirements and energy-saving requirements, has low production efficiency, and has old equipment with unstable process parameter control. In order to adapt to market competition, updating equipment is an effective way to improve production efficiency, improve product quality, and reduce production costs.

Transformation of equipment control mode: Strive to achieve the transformation from human-controlled equipment to human-controlled computers and computer-controlled equipment to make up for the defects of personnel quality. It is necessary to adapt to the development trend of automation and semi-automation of production equipment and various parameter collection functions.

3. The raw material supply mode should be transformed.

Raw material suppliers without scale will bring severe challenges to the stability of wire and cable product quality. Reducing the use of products from small general raw material suppliers in the region will be conducive to the improvement and control of product quality. In

the near future, raw material suppliers supporting wires and cables will also face a one-step integration. With the improvement of cable product quality and the strengthening of supervision measures, people's requirements for raw materials will be taken seriously, and the survival space of small-scale raw material production enterprises will be squeezed unprecedentedly. Therefore, pay attention to the development and transformation of small raw material production enterprises in the region. The future trend is that raw materials with large quantities and wide coverage (such as PVC.XLPE) will present large-scale suppliers.

In terms of policy, it is encouraged that large-scale or distinctive enterprises in the region establish their own R&D factories, change the current purchase of special materials to "develop" special cables, and turn it into a R&D model with independent intellectual property rights to develop special materials and special cables together.

4. Product varieties should be transformed For products with large quantities and wide coverage, the production capacity is already seriously oversupplied. For general enterprises, it is no longer realistic to transform and produce these products.

Encourage enterprises with first-class technical talents and capital strength in the region to accelerate the development of products that are urgently needed in the market or have strategic reserves, such as cable products and pipeline composite products needed in the deep sea, long-length power cables that meet the future urban pipeline corridors, and high-performance products using new conductor materials and new insulation sheath materials. Appropriate consideration should be given to the development of products with shortcomings in the region or acquisitions in other places, which is conducive to the scale construction and brand building of enterprises in the region.

For enterprises in the region with strong market development capabilities and certain technical strength, attention should be paid to changes and demands in the market segments, and efforts should be made to transform the product structure. For example: cables that meet special environmental requirements (laying methods, ambient temperature (high temperature, low temperature), acid resistance, alkali resistance, seawater resistance, fire resistance, flame retardant, low smoke and halogen-free, UV resistance, high pressure resistance, nuclear radiation resistance, water sealing (longitudinal, horizontal), seawater resistance, twisting resistance, bending resistance, optoelectronic composite, etc.).

5. Management concepts should be transformed to fully understand the importance and necessity of enterprises to establish big data. In the future, the entire industry, especially the places with concentrated industries, should guide enterprises to learn to use big data to manage enterprises in the process of enterprise management, and understand the following issues:

(1) What data should be established in the enterprise?

(2) How to connect the underlying big data (all data on production equipment) with the data in the ERP management system?

(3) What is the relationship between the underlying big data and "Made in China 2025"?

(4) Adapt to and learn to use "Internet +" and big data in management. In the future, Internet "+" and big data will be fully used in the industry, which will bring great convenience to various management work, production, testing, quality control and cost control of enterprises. We should pay attention to the application of big data in enterprise management, the application of "Internet +" in cable enterprises, and the construction of all data traceability systems.

(5) Learn to use "digital" to make decisions and manage the future network. The use of similar tools such as big data will greatly improve management efficiency. When making decisions, the leaders and managers of enterprises should change from "experience is decision-making" to "data-assisted decision-making" and then to "data is decision-making".

For example: relying on big data statistics and analysis to achieve zero inventory of raw materials; relying on Internet information and big data resources to make scientific decisions on new product development; using big data analysis of production equipment performance parameters to make decisions on equipment updates; using the Internet and big data can save decision-making time, streamline management personnel, and reduce costs.

6. The quality management concept should be transformed.

At present, various certificates represent product quality. This is based on full integrity. In today's society, when integrity is lacking, quality control is just a formality. In the region, we should innovate the quality supervision model, make full use of modern network tools such as the Internet and the Internet of Things, establish a traceability system for product production management and quality management, and create quality management characteristics for the wire and cable industry.

7. Talent concepts should be changed

(1) The concept of high-end talents in the wire and cable industry should be expanded. The wire and cable industry is a traditional manufacturing industry. Compared with high-end emerging industries (such as IT), there are great differences. There are many types of work that cannot be solved by high education. Cultivate and improve the skills and quality awareness of front-line employees and promote the spirit of "craftsmen". Front-line "craftsmen" are also high-end talents.

(2) Make full use of compound talents. When enterprises use and introduce talents, in order to adapt to the needs of industry integration and development, they should pay more attention to the use of compound talents, such as: professional knowledge + market development capabilities, professional knowledge + big data application, professional knowledge + Internet knowledge, professional knowledge + various types of enterprise management, professional knowledge + quality control, etc. These compound talents will have the opportunity to show their talents in the future. Talents cannot be copied, and enterprises must respect talents. Only by respecting and using talents well can enterprises grow and develop.